California and Arizona both have anti-deficiency laws in place to protect homeowners from having to pay the difference between the mortgage balance and the sale price if the house is foreclosed upon. However, some consumers have complained that the deficiencies are included in their credit reports — despite lenders being legally prohibited from collecting any amount more than recovered in a non-judicial foreclosure sale.

How Do Anti-Deficiency Laws Protect Homeowners?

In many cases, if a borrower is delinquent on their mortgage, the lender will take the title back to the house and sell it in a foreclosure sale. Often, when this occurs, there is a deficiency between the amount owed on the Note and the foreclosure price. In states with anti-deficiency laws — such as California, Arizona, and several others — a lender may not be permitted to collect the difference.

Specifically, in Arizona, the anti-deficiency statute protects those with a mortgage on a one or two-family home situated on 2.5 acres of land or less.

Lenders may be permitted to pursue a deficiency if the property is foreclosed upon in a judicial sale in California. However, the lender will not be able to obtain a deficiency judgment if the loan was used to purchase an owner-occupied one to four-family home or if the seller financed the home.

Additionally, it’s essential to be aware of certain exceptions to the anti-deficiency laws. For example, these protections typically do not extend to mortgage fees, second mortgages or homes that are not the primary residence.

What Can You Do if Your Credit Score Was Affected by Mortgage Issues?

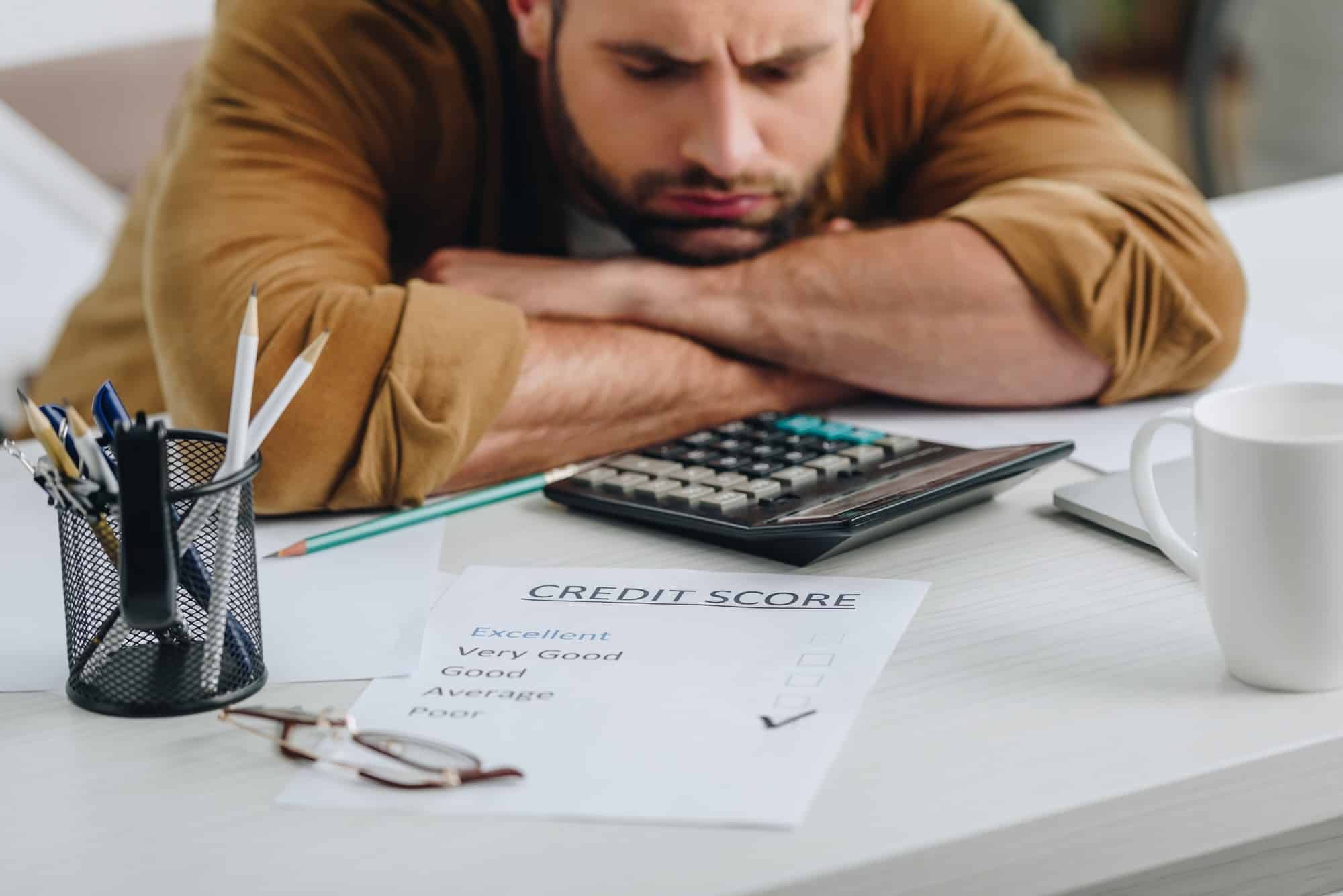

Unfortunately, late mortgage payments, short sales, and foreclosures can all have a significant impact on your credit score. According to The Truth About Mortgage, a mortgage payment that is late by 30 days or more can drop your credit score by 60 to 100 points.

Unfortunately, late mortgage payments, short sales, and foreclosures can all have a significant impact on your credit score. According to The Truth About Mortgage, a mortgage payment that is late by 30 days or more can drop your credit score by 60 to 100 points.

If you believe your lender or mortgage servicer made an error, you can contact the bank or lender to dispute the issue. If they agree to remedy the error, you should be notified of the correction in writing. The servicer should also inform the credit bureau of the error.

Lawyers are currently investigating consumers’ claims concerning whether late mortgage payments and foreclosures are being appropriately handled by lenders and credit reporting agencies in California and Arizona. If this has happened to you, an experienced attorney can best advise you concerning your legal rights and remedies.

Critically, if you are an Arizona homeowner who has had negative entries on your credit report or a lowered credit score due to a missed mortgage payment, you might be entitled to compensation. Similarly, those in California who have had derogatory entries on their credit reports due to a foreclosure or short sale may also be eligible to receive monetary recovery.

ATTORNEY ADVERTISING

Top Class Actions is a Proud Member of the American Bar Association

LEGAL INFORMATION IS NOT LEGAL ADVICE

Top Class Actions Legal Statement

©2008 – 2026 Top Class Actions® LLC

Various Trademarks held by their respective owners

This website is not intended for viewing or usage by European Union citizens.