Consumers in America have various protections against credit card fraud and identity theft, due to state and federal policies retail companies must follow.

Consumers in America have various protections against credit card fraud and identity theft, due to state and federal policies retail companies must follow.

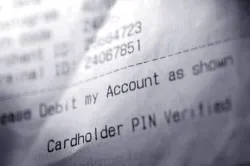

One of these policies is the Fair and Accurate Credit Transactions Act (FACTA), which requires all retailers to perform truncation on consumers’ credit card receipts and debit card receipts. Merchants who do not follow FACTA policy, could face $1,000 per violation and further penalties depending on the severity of the case.

This policy was passed by Congress in 2003 as an amendment to the Fair Credit Reporting Act, to combat the rising problem of credit card fraud and identity theft. The process of truncation, the primary rule of FACTA, shortens the amount of numbers of shown on a customer’s credit card receipt or debit card receipt as well as prohibits the printing of the card’s expiration date.

FACTA policy states that no merchant accepting credit or debit cards for payment transactions, shall print no more than the last five number of the card and must completely omit the expiration date on a debit card receipt or credit card receipt.

FACTA policy applies to all electronically printed customer receipts from cash registers, self service kiosks, and restaurant tickets. However, this policy does not apply to any handwritten receipts or imprinted copy of the card.

Overview of FACTA Truncation Policy

Truncation is a vital part of customer security that all business, large and small, should follow to lower the chances of identity theft.

When FACTA was first enacted in 2003, it took several violations and lawsuits for businesses to understand that this policy is necessary for customer security. When Congress first passed FACTA to combat identity theft, the number of businesses hit with truncation violations was highly unexpected.

Over the years, the courts have distinguished between willful and negligible FACTA violations. Willful FACTA violations indicate the company may have acted “recklessly” against the customers, by not protecting vital identifiable information.

When first enacted, most merchants defend themselves against FACTA allegations by stating they were unaware that the rule existed or that there was a problem with their transaction systems. With FACTA now ten years old, merchants are now expected to have adapted to current policy.

Consumers are advised to verify that their transaction system follows proper truncation, protecting them against credit card fraud and identity theft. If you noticed a credit card receipt or debit card receipt with a FACTA violation, your may be eligible to file legal action against the merchants.

Legal experts advise potential FACTA claimants to keep documentation that supports the complaints, including the alleged receipts. Potential claimants should file legal action as soon as possible, as the statue of limitations only allows two years to report the violation two years after discovery.

Free FACTA Class Action Lawsuit Investigation

If you made one or more purchases and the retailer provided you with a receipt that contained more than the last five digits of your credit or debit card number or the expiration date, you may be eligible for a free class action lawsuit investigation and to pursue compensation for these FACTA violations.

ATTORNEY ADVERTISING

Top Class Actions is a Proud Member of the American Bar Association

LEGAL INFORMATION IS NOT LEGAL ADVICE

Top Class Actions Legal Statement

©2008 – 2026 Top Class Actions® LLC

Various Trademarks held by their respective owners

This website is not intended for viewing or usage by European Union citizens.