Identity theft and credit card fraud have become real threats as, with each passing year, it becomes easier to use a debit or credit card to make purchases virtually anywhere.

Identity theft and credit card fraud have become real threats as, with each passing year, it becomes easier to use a debit or credit card to make purchases virtually anywhere.

In an attempt to protect customers from these risks, Congress enacted the Fair and Accurate Credit Transaction Act (FACTA). Customers are protected under these federal laws from retailers who might be placing consumers at extra risk. However, credit card users can also take extra precautions of their own in order to minimize the potential of identity theft even further.

Credit Card Safety Tips

There are many ways consumers can take measures into their own hands in order to reduce the risk of credit card fraud.

- Carry credit and debit cards separately in order to reduce the risk in case someone steals your purse or wallet

- Contact your card issuer if you will be traveling

- Make sure to draw a line through any blank “tip” spaces above the total

- Carry only the card you need for a certain transaction

- Check your transactions often either online or through statements

- Destroy all receipts once you’ve reconciled transactions

- Contact your card issuer if your address has changed

- Make sure you get your credit card back after a transaction

- Unless you are certain a company is trustworthy, do not give your account number over the phone

- Immediately report any lost, stolen, or compromised cards to the credit card company

FACTA Laws Explained

Millions of customers are affected by identity theft and credit card fraud in the U.S. each year. For that reason, Congress has established certain rules that apply to all businesses, retailers, and even self-service kiosks when it comes to issuing credit or debit card receipts.

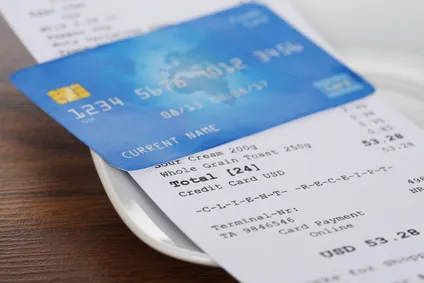

Identity thieves can easily piece together a full credit or debit card number if it isn’t protected well enough. Therefore, FACTA laws require that “no person that accepts credit cards or debit cards for the transaction of business shall print more than the last 5 digits of the card number.”

This means retailers and other businesses must hide the other digits in a variety of ways but typically by using symbols including * and # instead of the actual numbers. A FACTA violation of this credit card receipt rule could look like any of the following examples.

Example 1: **** **** **77 ****

Example 2: 44** **** **** 5555

Example 3: **** **11 **** 8888

As you can see, a FACTA violation may occur even if less than five numbers are shown on a receipt. The law is very specific that it must include no more than the LAST five digits of the card number.

Another common FACTA violation is in regards to the expiration date of the card. The federal law requires that businesses should not print the expiration date “upon any receipt provided to the cardholder at the point of the sale or transaction.” This FACTA violation could appear in the following forms:

EXP: 0218

EXP: 02/18

EXP: 02/2018

FACTA Lawsuits

Customers who find that a business printed a receipt that showed an expiration date or more than the last five digits of a credit or debit card number may have legal claim. FACTA violations fees typically range between $100 to $1,000 per violation. Contact a FACTA attorney to find out if you should file a FACTA lawsuit as an individual or join a FACTA class action lawsuit.

Free FACTA Class Action Lawsuit Investigation

If you made one or more purchases and the retailer provided you with a receipt that contained more than the last five digits of your credit or debit card number or the expiration date, you may be eligible for a free class action lawsuit investigation and to pursue compensation for these FACTA violations.

ATTORNEY ADVERTISING

Top Class Actions is a Proud Member of the American Bar Association

LEGAL INFORMATION IS NOT LEGAL ADVICE

Top Class Actions Legal Statement

©2008 – 2026 Top Class Actions® LLC

Various Trademarks held by their respective owners

This website is not intended for viewing or usage by European Union citizens.

Suing for unpaid wages in California: Recover unpaid overtime, back pay and more

April 2, 2026 | Legal News